All Categories

Featured

[/video]

This can lead to much less benefit for the insurance policy holder contrasted to the economic gain for the insurance provider and the agent.: The illustrations and presumptions in advertising and marketing materials can be deceptive, making the policy appear a lot more appealing than it might really be.: Realize that economic consultants (or Brokers) make high commissions on IULs, which might influence their suggestions to offer you a plan that is not suitable or in your finest interest.

A lot of account choices within IUL items ensure among these limiting variables while allowing the other to float. The most usual account alternative in IUL policies features a floating yearly rate of interest cap in between 5% and 9% in current market problems and an assured 100% participation rate. The passion made equates to the index return if it is much less than the cap however is covered if the index return goes beyond the cap price.

Various other account alternatives may include a floating engagement rate, such as 50%, without cap, indicating the passion credited would be half the return of the equity index. A spread account debts interest above a floating "spread out price." For example, if the spread is 6%, the interest credited would be 15% if the index return is 21% however 0% if the index return is 5%.

Passion is usually credited on an "annual point-to-point" basis, suggesting the gain in the index is determined from the point the costs got in the account to specifically one year later on. All caps and involvement rates are after that used, and the resulting interest is credited to the plan. These rates are readjusted each year and used as the basis for computing gains for the list below year.

The insurance firm gets from an investment bank the right to "buy the index" if it exceeds a specific degree, recognized as the "strike rate."The provider can hedge its capped index obligation by buying a call option at a 0% gain strike price and creating a telephone call choice at an 8% gain strike rate.

Index Universal Life Insurance Cost

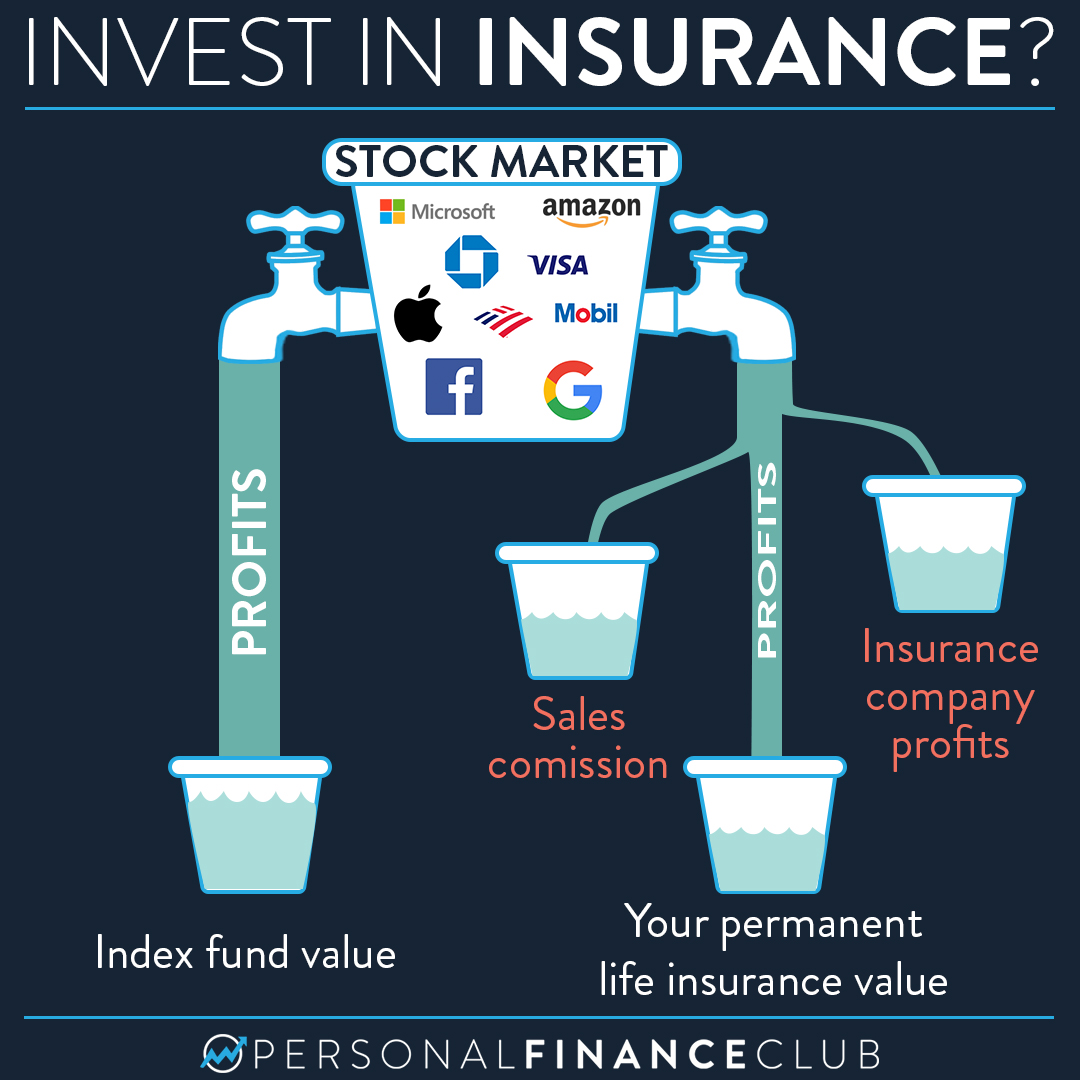

The spending plan that the insurance coverage company has to acquire choices relies on the return from its basic account. As an example, if the carrier has $1,000 internet premium after deductions and a 3% yield from its general account, it would certainly assign $970.87 to its basic account to grow to $1,000 by year's end, utilizing the staying $29.13 to buy options.

The 2 biggest variables affecting drifting cap and engagement rates are the returns on the insurance policy firm's general account and market volatility. As returns on these assets have decreased, carriers have actually had smaller sized budgets for buying choices, leading to lowered cap and engagement prices.

Providers generally highlight future performance based on the historical efficiency of the index, applying current, non-guaranteed cap and involvement prices as a proxy for future performance. This method might not be practical, as historical estimates commonly show higher previous rate of interest rates and presume consistent caps and engagement rates in spite of varied market problems.

A better strategy may be designating to an uncapped involvement account or a spread account, which entail getting relatively low-cost choices. These techniques, nevertheless, are much less stable than capped accounts and might need constant changes by the service provider to mirror market conditions accurately. The story that IULs are traditional products supplying equity-like returns is no longer sustainable.

With reasonable expectations of options returns and a diminishing budget for purchasing alternatives, IULs might offer marginally higher returns than traditional ULs but not equity index returns. Possible customers should run images at 0.5% over the rate of interest credited to standard ULs to analyze whether the plan is correctly moneyed and with the ability of supplying promised performance.

As a trusted companion, we collaborate with 63 premier insurance policy business, guaranteeing you have access to a diverse array of alternatives. Our services are entirely free, and our expert consultants supply unbiased recommendations to assist you locate the very best coverage customized to your demands and budget plan. Partnering with JRC Insurance coverage Team implies you get personalized service, competitive prices, and assurance recognizing your financial future remains in capable hands.

Dave Ramsey Index Universal Life

We aided countless family members with their life insurance policy needs and we can aid you too. Composed by: Louis has remained in the insurance organization for over thirty years. He focuses on "high risk" cases as well as even more complex protections for lengthy term treatment, handicap, and estate preparation. Specialist reviewed by: High cliff is a qualified life insurance agent and among the proprietors of JRC Insurance coverage Team.

In his spare time he takes pleasure in costs time with household, traveling, and the great outdoors.

Variable plans are financed by National Life and distributed by Equity Solutions, Inc., Registered Broker/Dealer Associate of National Life Insurance Policy Firm, One National Life Drive, Montpelier, Vermont 05604. Be certain to ask your financial advisor concerning the lasting treatment insurance coverage plan's attributes, benefits and costs, and whether the insurance policy is ideal for you based on your financial situation and objectives. Handicap income insurance usually supplies monthly revenue benefits when you are unable to function due to a disabling injury or illness, as specified in the policy.

Money worth expands in an universal life policy via attributed passion and reduced insurance coverage expenses. 6 Policy advantages are decreased by any type of superior lending or loan interest and/or withdrawals. Dividends, if any kind of, are influenced by plan lendings and car loan rate of interest. Withdrawals over the price basis might result in taxable common income. If the plan gaps, or is given up, any type of impressive loans thought about gain in the plan may be subject to normal earnings tax obligations. This adjustment, subject to the cap price(currently 10.5%)and flooring(presently 4%), may declare or unfavorable based on the S&P 500 rate return index efficiency. Negative market performance can create negative dividend adjustments which may cause reduced general money worths than would certainly or else have accruedhad the IPF rider not been selected. The expense of the IPF biker is presently 2 %with a guaranteed rate of 3 %on the IPF section of the plan. Policy loans versus, or withdrawals of, worths assigned to the IPF might adversely influence rider efficiency. Option of the IPF may restrict the use of certain dividend choices. You ought to take into consideration the financial investment goals, threats, costs and costs of the investment firm carefully prior to investing. Please call your investment professional or call 888-600-4667 for a program, which contains this and other essential details. Annuities and variable life insurance policy released by The Guardian Insurance Policy & Annuity Company, Inc.(GIAC ), a Delaware firm. Are you in the market for life insurance policy? If so, you may be wondering which sort of life insurance policy product is ideal for you. There are a variety of various kinds of life insurance policy around, each with its very own benefits and disadvantages. Figuring out which is right for you will certainly depend upon a number of aspects, like your life insurance policy goals, your monetary dedicationto paying costs on schedule, your timeline for making payments, and much more. This money worth can later be withdrawn or borrowed against *. Significantly, Universal Life insurance policy plans supply insurance policy holders with a death advantage. This death advantage builds up gradually with each premium paid on schedule. Upon the insurance holder's passing, this death benefit will certainly be paid to recipients called in the plan contract. 1Loans, partial surrenders and withdrawals will decrease both the abandonment worth and death benefit. Under certain situations, policy car loans and withdrawals might be subject to income taxation. This info is exact unless the plan is a changed endowment contract. 2Agreements/riders may be subject to additional costs and limitations. Indexed Universal Life insurance policy is made first and foremost to give life insurance coverage protection. Taxpayers should seek the suggestions of their own tax obligation and lawful consultants regarding any tax and lawful problems appropriate to their details circumstances. This is a general communication for informational and educational functions. The products and the info are not designed or planned, to be appropriate to anyone's individual conditions. A taken care of indexed global life insurance (FIUL)policy is a life insurance policy item that supplies you the opportunity, when properly moneyed, to get involved in the development of the marketplace or an index without directly buying the market. At the core, an FIUL is created to provide security for your liked ones on the occasion that you die, yet it can likewise supply you a broad range of benefits while you're still living. The key distinctions between an FIUL and a term life insurance policy plan is the adaptability and the benefits outside of the death advantage. A term policy is life insurance policy that assures payment of a mentioned death benefit during a specified time period( or term )and a given premium. Once that term expires, you have the choice to either restore it for a new term, end or convert it to a premiuminsurance coverage. An FIUL can be made use of as a safety and security web and is not a substitute for a long-term healthcare plan. Make sure to consult your financial professional to see what kind of life insurance and advantages fit your requirements. A benefit that an FIUL uses is comfort. You can rest guaranteed that if something happens to you, your family members and loved ones are dealt with. You're not subjecting your hard-earned cash to a volatile market, developing for on your own a tax-deferred asset that has built-in protection. Historically, our firm was a term service provider and we're devoted to offering that business yet we have actually adjusted and re-focused to fit the transforming requirements of consumers and the needs of the industry. It's a market we've been committed to. We have actually dedicated sources to creating several of our FIULs, and we have a focused initiative on being able to give solid services to consumers. FIULs are the fastest growing section of the life insurance policy market. It's a room that's expanding, and we're mosting likely to maintain it. On the various other hand, a It supplies tax advantages and usually company matching payments. As you will discover right here, these are not replace items and are suited for distinct needs and goals. A lot of everybody needs to build financial savings for retirement, and the demand forever insurance will certainly rely on your goals and monetary situation. Payments to a 401(k) can be made with either pre or post tax obligation dollars(using Roth if your plan permits). Cash after that can grow taxdeferredup until withdrawal during retirement, or when it comes to Roth payments, taxfree, revenues and all. Better, most employers provide a matching payment that the staff member would not or else receive unless they take part in their 401(k)plan.

{kind=link}

Latest Posts

Indexed Universal Life Unleashed

Aviva Indexed Universal Life Insurance Reviews

Vul Vs Iul